Morocco’s e-commerce sector exhibits sustained growth, marked by the emergence of new marketplaces, the proliferation of social commerce, and expanding digital adoption.

Notwithstanding this expansion, the Moroccan market for last-mile logistics remains in an incipient phase of development.

A comprehensive understanding of this market structure is paramount for any entity establishing digital commerce operations within the country.

A) A Market Volume of 100,000 Parcels Daily

Industry consensus estimates Morocco’s e-commerce volume at approximately 100,000 parcels per day, a figure that excludes quick commerce and food delivery services.

This volume translates to an estimated 35–40 million parcels annually.

A comparative analysis with other markets underscores the difference in scale:

- France: approx 1.5 billion parcels per year

- United Kingdom: approx 4 billion parcels per year

- United States: exceeding 20 billion parcels per year

Even amongst developing economies, Morocco’s market size is relatively modest. The inherent conclusion is that the market is at the genesis of its growth trajectory.

B) Social Commerce as a Catalyst for Digital Sales

In contrast to Western markets primarily driven by structured e-commerce platforms, Morocco’s digital commerce ecosystem is significantly influenced by social commerce.

A substantial proportion of transactions originate from:

- Instagram and Facebook pages

- WhatsApp correspondence

- Marketplace platforms

- Retailer-owned online storefronts

For numerous merchants, the purchasing process is not a standardized website checkout, but rather a dialogue.

While this model facilitates swift merchant onboarding, it concurrently generates operational complexities for logistics networks, including fragmented order pipelines and volatile volumes.

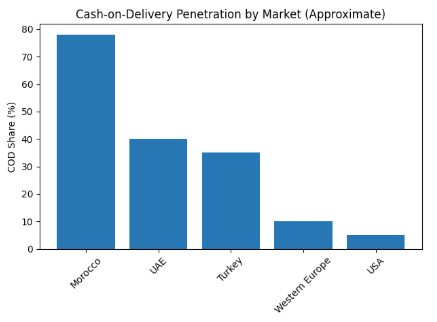

C) Cash on Delivery Continues to Define the Ecosystem

The most salient characteristic of Moroccan e-commerce remains the predominance of Cash on Delivery (COD).

Currently, 75–80% of e-commerce transactions are still executed via COD.

While this payment mechanism has been instrumental in cultivating consumer trust in online commerce, it simultaneously introduces structural inefficiencies across the entire last-mile value chain.

COD directly impacts:

- Delivery success ratios

- Merchandise return rates

- Operating expenditures

In many Moroccan operations, first-attempt delivery success rates typically range between 65–75%, a lower bound compared to the 90–95% observed in card-dominant markets.

This disparity necessitates heightened operational complexity and results in substantially elevated logistics costs.

D) Persistent Structural Obstacles

Despite advancements in recent years, several structural challenges continue to characterize the Moroccan last-mile ecosystem.

Addressing systems lack standardization. Delivery personnel frequently rely on telephonic communication or subjective directional guidance to ascertain customer locations.

Operational fragmentation is pronounced. The market comprises national carriers, independent private logistics firms, and nascent last-mile startups, often operating with disparate standards and service level agreements.

Consumer preferences still prioritize flexibility over commitment. The prerogative to decline delivery or remit payment only after product inspection remains deeply embedded in consumer purchasing behavior.

E) A Market Full of Opportunities

Notwithstanding these constraints, Morocco’s last-mile ecosystem is poised to enter a transformative phase.

Several fundamental drivers indicate robust long-term growth potential:

- Augmenting smartphone penetration rates

- Expansion of digital payment methods

- Growth of marketplace platforms

- Escalating consumer expectations regarding delivery speed and dependability

As these forces converge, last-mile logistics is set to become one of the most critical strategic enablers of Moroccan e-commerce.

The successful enterprises will be those capable of integrating technology, operational rigor, and financial flexibility in a market where logistics constitutes both the primary constraint and the greatest area of potential.